Why the federal funds rate has limited impact on housing recovery? When the chair of the U.S. Federal Reserve speaks about interest rates, financial markets tend to listen closely. Yet recent remarks suggesting that rate cuts may not significantly improve conditions in the housing market reflect a more sobering assessment of the limits of monetary policy. At the center of that assessment is the federal funds rate, the benchmark interest rate that anchors borrowing costs across the economy.

For years, housing has been among the most interest-sensitive sectors in the United States. Lower rates traditionally stimulate demand by reducing mortgage costs, while higher rates cool overheated markets. But the current environment, shaped by supply shortages, high construction costs, and shifting demographics, has complicated that familiar relationship. According to policymakers, adjustments to the federal funds rate alone are unlikely to resolve those deeper challenges.

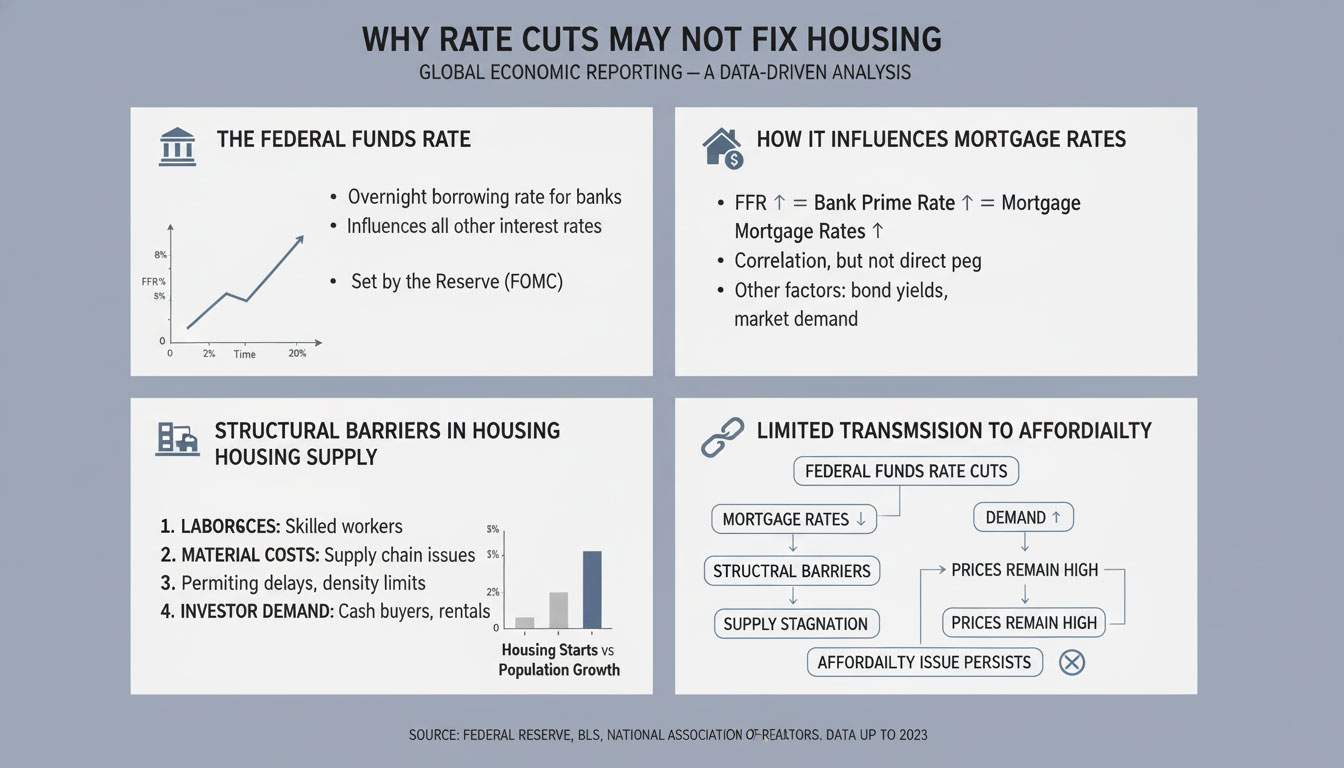

Understanding the Role of the Federal Funds Rate

The federal funds rate is the interest rate at which banks lend reserves to each other overnight. Set by the Federal Open Market Committee, it serves as the foundation for broader financial conditions, influencing everything from consumer loans to corporate borrowing. Mortgage rates, while not directly tied to it, tend to move in response to expectations about future rate policy.

In theory, reducing the federal funds rate should ease credit conditions, making mortgages more affordable and encouraging home purchases. In practice, however, mortgage rates also reflect long-term bond yields, inflation expectations, and global capital flows. As a result, the transmission from policy rate cuts to housing affordability can be uneven and delayed.

Why Housing Is Not Responding as Before

The housing sector today faces constraints that go beyond borrowing costs. Even if the federal funds rate were lowered, supply-side pressures would remain. Years of underbuilding following the global financial crisis have left many regions with insufficient housing stock. Zoning restrictions, labor shortages in construction, and elevated material costs further limit new supply.

Demand dynamics have also shifted. Higher home prices over the past decade have pushed affordability to historically strained levels. For many first-time buyers, even modest reductions in mortgage rates may not offset high prices and down payment requirements. This is one reason policymakers caution against expecting rate cuts to produce immediate or dramatic changes.

Key Information Table On: Shaping the Housing Market

| Factor | Current Condition | Impact on Housing |

|---|---|---|

| Federal funds rate | Elevated relative to pre-pandemic levels | Influences mortgage costs indirectly |

| Housing supply | Structurally constrained | Limits availability despite demand |

| Construction costs | Remain high | Slows new home development |

| Household incomes | Growing unevenly | Weakens affordability |

| Demographics | Shifting buyer preferences | Alters demand patterns |

These dynamics underscore why the federal funds rate, while important, is only one piece of a much larger puzzle.

Monetary Policy Versus Structural Constraints

Federal Reserve officials have increasingly emphasized that monetary policy is a blunt tool. It is effective at managing inflation and stabilizing financial conditions, but it cannot directly address supply shortages or regulatory barriers. In housing, those structural issues dominate the outlook.

Lowering the federal funds rate could, over time, ease financing conditions for builders and buyers alike. But without parallel improvements in supply, the risk is that prices simply adjust upward, leaving affordability largely unchanged. This concern has become more pronounced as housing inflation remains a persistent component of broader price pressures.

The Mortgage Rate Disconnect

One reason housing remains sluggish even amid expectations of future easing is the weak link between the federal funds rate and mortgage rates. Thirty-year fixed mortgage rates are more closely tied to long-term Treasury yields, which incorporate expectations about inflation and fiscal policy.

If investors believe inflation will remain elevated or that government borrowing will stay high, long-term yields may not fall significantly, even if the policy rate is reduced. In such scenarios, cuts to the federal funds rate may offer limited relief to prospective homebuyers.

Housing Affordability as a Policy Challenge

Affordability has emerged as one of the defining economic issues of the current cycle. High prices, elevated interest rates, and limited inventory have combined to push homeownership further out of reach for many households. While the federal funds rate influences borrowing costs, it does not directly address wage growth disparities or regional housing shortages.

This reality has prompted calls for a broader policy response. Measures such as zoning reform, incentives for affordable housing development, and targeted support for first-time buyers are increasingly seen as necessary complements to monetary policy.

Regional Variations in Housing Sensitivity

Not all housing markets respond to interest rates in the same way. In some regions, where supply is more flexible and prices are lower, changes to the federal funds rate can still have a noticeable impact. In high-cost metropolitan areas, however, affordability constraints dominate, muting the effect of rate adjustments.

These regional disparities complicate the Federal Reserve’s task. A policy stance calibrated for national conditions may be too restrictive for some areas and insufficient for others. This further limits the ability of the federal funds rate to serve as a precise lever for housing outcomes.

Financial Stability Considerations

Another reason for caution is financial stability. Rapid or aggressive cuts to the federal funds rate could reignite speculative behavior in housing markets, particularly if supply remains constrained. Policymakers remain mindful of the risks associated with asset bubbles, especially given the lessons of past cycles.

By signaling that rate cuts are not a cure-all for housing, Federal Reserve leadership aims to manage expectations and reinforce the idea that sustainable housing growth depends on fundamentals, not just cheaper credit.

The Broader Economic Context

Housing does not operate in isolation. It interacts with labor markets, consumer confidence, and broader economic growth. If economic uncertainty persists, households may remain cautious about large purchases, regardless of movements in the federal funds rate.

Moreover, tighter credit standards and elevated household debt levels can further dampen the response to rate changes. In such an environment, even meaningful reductions in the policy rate may translate into only modest gains in housing activity.

What This Means for Buyers and Sellers

For buyers, the message is nuanced. While future adjustments to the federal funds rate could improve financing conditions at the margin, they are unlikely to restore the ultra-low mortgage rates of the past decade. Affordability challenges are expected to persist, particularly in supply-constrained markets.

For sellers, limited inventory may continue to support prices, even if demand remains subdued. This balance helps explain why housing markets have not seen the sharp corrections that some predicted when rates rose.

Implications for Long-Term Housing Policy

The growing consensus among policymakers is that housing affordability cannot be solved through monetary policy alone. The federal funds rate can influence demand, but supply-side reforms are essential for lasting improvement.

This shift in emphasis may shape future debates at the intersection of economic policy and housing. As the Federal Reserve maintains its focus on inflation and employment, responsibility for housing outcomes increasingly falls to lawmakers and local governments.

A Measured Outlook

The acknowledgment that rate cuts may not dramatically improve housing conditions reflects a more realistic appraisal of economic constraints. It also underscores the Federal Reserve’s commitment to transparency. By clarifying the limits of the federal funds rate, policymakers help households, investors, and builders make more informed decisions.

Rather than promising quick fixes, the message points toward gradual adjustment and structural reform. In that sense, it marks a departure from the assumption that monetary easing alone can revive housing demand.

The housing sector’s struggles illustrate the boundaries of central bank influence. While the federal funds rate remains a powerful tool for guiding financial conditions, its ability to resolve complex, supply-driven challenges is limited. As policymakers signal restraint in their expectations, attention is shifting toward longer-term solutions that extend beyond interest rates.

For now, the outlook suggests moderation rather than transformation. Housing recovery, if it comes, is likely to be shaped less by the timing of rate cuts and more by the pace of structural change across the economy.