What Are Mortgage Rates and How Do They Work? For the vast majority of prospective homeowners, the path to property ownership runs directly through the complex infrastructure of the mortgage market. While the listing price of a home dominates headlines, it is the underlying cost of borrowing—the interest rate—that ultimately dictates affordability and market accessibility. Understanding mortgage rates is not merely a bureaucratic necessity; it is a fundamental requirement for financial literacy in the modern economy.

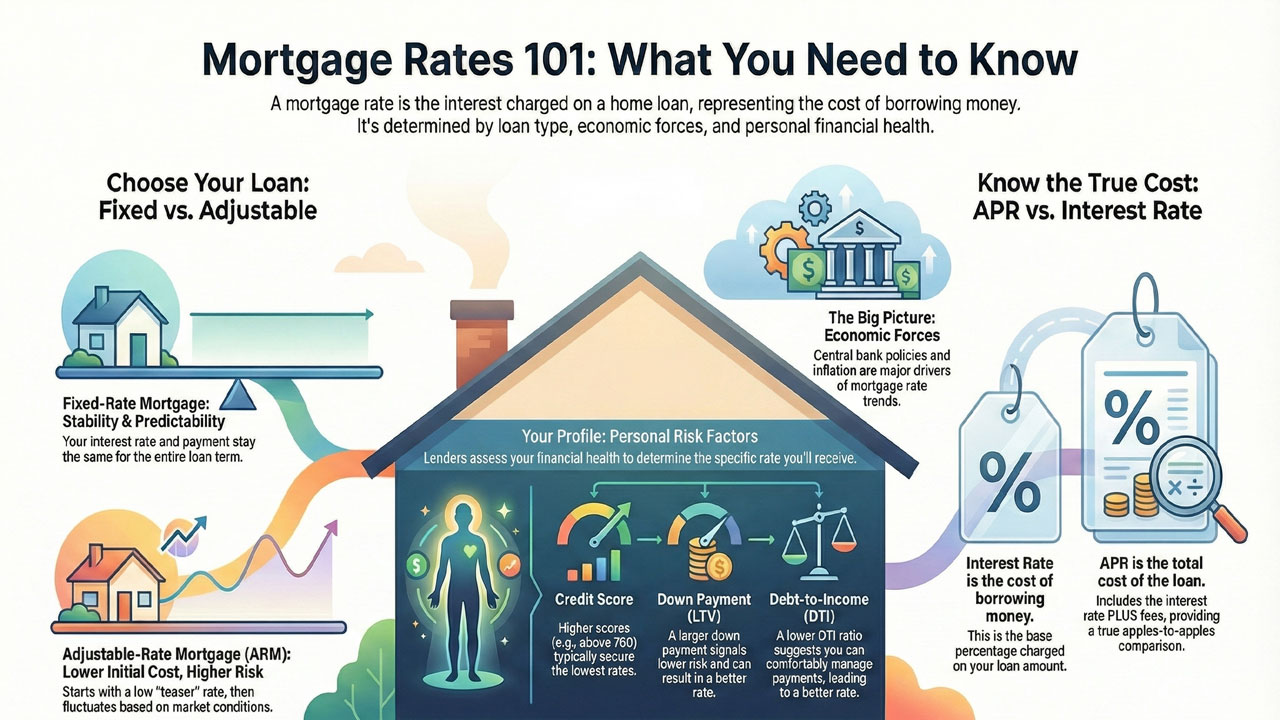

A mortgage rate is, in essence, the interest charged on a loan used to purchase a property. It represents the cost of “renting” money from a lender. However, unlike a simple rental agreement, the determination of this rate is a sophisticated process influenced by a convergence of global economic forces, central bank policies, and individual borrower risk profiles. To navigate this landscape effectively, one must look beyond the percentage point and understand the machinery that drives it.

The Fundamental Mechanics : Interest vs. Principal

When a financial institution lends capital for a home purchase, the repayment is structured to cover two distinct components: the principal (the original amount borrowed) and the interest (the lender’s profit for taking the risk). The mortgage rate applies specifically to the principal balance.

In the early years of a typical loan term, the majority of the monthly payment is allocated toward interest rather than reducing the principal. This structure, known as amortization, ensures that the lender recuperates their risk premium early in the lifecycle of the loan. As the years progress, the scale tips, and a larger portion of the payment begins to erode the principal debt. Therefore, even a fractional difference in the rate can result in tens of thousands of dollars in variance over the life of a thirty-year loan.

Fixed vs. Adjustable : The Structural Dichotomy

Borrowers are generally presented with two primary architectural frameworks for their loans: the fixed-rate mortgage and the adjustable-rate mortgage (ARM).

The Stability of Fixed Rates

The fixed-rate mortgage is the bedrock of the American housing market and is increasingly popular globally. As the nomenclature suggests, the interest rate remains static throughout the duration of the loan, typically 15 or 30 years. This offers the borrower immunity against economic volatility. Regardless of inflation spikes or shifts in monetary policy, the monthly principal and interest payment remains constant. This predictability aids in long-term financial planning, though it often comes with a slightly higher initial rate compared to adjustable alternatives to compensate the lender for assuming long-term interest rate risk.

The Dynamics of Adjustable Rates (ARMs)

Conversely, an adjustable-rate mortgage features an interest rate that fluctuates based on a specific market index. These loans typically begin with a “teaser” period—often 5, 7, or 10 years—during which the rate is fixed and usually lower than prevailing fixed-rate averages. Once this period expires, the rate resets annually or semi-annually based on market conditions. While ARMs can offer lower initial costs, they transfer the risk of rising interest rates from the lender to the borrower. If the broader economic environment shifts toward high inflation, an ARM borrower could see their monthly obligations surge significantly.

Macroeconomic Drivers: What Moves the Needle?

It is a common misconception that lenders set mortgage rates arbitrarily. In reality, lenders are reacting to broader economic signals. While central banks, such as the Federal Reserve in the United States or the Bank of England, do not set consumer mortgage rates directly, their influence is undeniable.

When a central bank adjusts the federal funds rate—the rate at which banks lend to one another overnight—it creates a ripple effect. A higher federal funds rate makes borrowing more expensive for banks, a cost that is invariably passed down to consumers. Furthermore, mortgage rates are inextricably linked to the bond market, specifically long-term government bonds like the 10-year U.S. Treasury note.

Investors view government bonds as “safe” assets. When the economy is robust and investors feel confident, they tend to move money out of bonds and into riskier assets like stocks. This sell-off lowers bond prices and raises their yields. Because mortgage-backed securities (MBS) must compete with government bonds for investor capital, mortgage rates generally rise in tandem with bond yields.

The Inflation Equation

Inflation is the arch-nemesis of long-term debt. If a lender provides funds at 4% interest, but inflation is running at 5%, the lender is effectively losing purchasing power over time. Consequently, when inflationary pressures mount, lenders demand higher interest rates to preserve the real value of their returns. This dynamic explains why periods of high inflation are almost historically accompanied by elevated borrowing costs.

The Borrower’s Profile : Assessing Risk

While the global economy sets the baseline, the specific rate offered to an individual borrower is determined by a rigorous assessment of risk. Lenders utilize a matrix of factors to calculate the probability of default, adjusting the interest rate—often referred to as “risk-based pricing”—accordingly.

What Are Mortgage Rates?

| Factor | Description | Impact on Rate |

|---|---|---|

| Credit Score | A numerical representation of creditworthiness based on credit history. | High Impact: Scores above 760 typically secure the lowest rates (“prime”), while scores below 620 trigger significantly higher premiums. |

| Loan-to-Value (LTV) | The ratio of the loan amount to the appraised value of the property. | Medium Impact: Larger down payments (lower LTV) signal lower risk to the lender, often resulting in better rate offers. |

| Debt-to-Income (DTI) | The percentage of gross monthly income that goes toward paying debts. | Medium Impact: A lower DTI (typically under 36%) suggests the borrower has sufficient cash flow to manage the mortgage, leading to favorable rates. |

| Loan Type | The specific loan program (e.g., Conventional, FHA, VA, Jumbo). | Variable Impact: Government-backed loans may offer lower rates but require mortgage insurance, altering the effective cost. |

| Property Use | Intended use of the home (Primary residence vs. Investment). | Medium Impact: Investment properties generally carry higher rates due to a historically higher likelihood of default during financial hardship. |

APR vs. Interest Rate: The Crucial Distinction

A frequent point of confusion for novice homebuyers is the discrepancy between the advertised interest rate and the Annual Percentage Rate (APR). While these figures are related, they are not identical.

The interest rate reflects the cost of borrowing the principal sum. The APR, however, is a broader measure of the total cost of the loan on a yearly basis. It includes the interest rate plus other charges such as mortgage broker fees, discount points, and closing costs.

From a regulatory standpoint, the APR is intended to provide a transparent, apples-to-apples comparison between lenders. A lender might advertise a highly attractive interest rate but load the loan with excessive fees. In such a scenario, the APR would be significantly higher than the interest rate, alerting the consumer to the true cost of the financing. When shopping for mortgage rates, savvy borrowers focus on the APR to gauge the true competitiveness of an offer.

The Role of Discount Points

In the pursuit of lower monthly payments, borrowers often encounter the option to purchase “discount points.” A point is essentially a fee paid upfront at closing—typically 1% of the loan amount—in exchange for a permanent reduction in the interest rate.

This practice, known as “buying down the rate,” can be financially advantageous for those who intend to stay in the property for a long duration. The upfront cost is eventually recuperated through monthly savings. However, for buyers who anticipate moving or refinancing within a few years, the break-even point may never be reached, rendering the purchase of points a financial loss.

Global Variations in Lending

While the principles of risk and return are universal, the structure of mortgage markets varies significantly across borders.

- United States: Uniquely characterized by the prevalence of the 30-year fixed-rate mortgage, largely due to government-sponsored enterprises like Fannie Mae and Freddie Mac that securitize these loans, guaranteeing liquidity in the market.

- United Kingdom: Borrowers often prefer “fixed terms” of two to five years. Once this period ends, the borrower usually refinances or reverts to the lender’s standard variable rate, making the UK market more sensitive to short-term interest rate changes.

- Canada: Similar to the UK, Canadian mortgages often have terms (typically 5 years) that are shorter than the amortization period (25 years). The interest rate is renegotiated at the end of each term.

- Europe: Varies by country, but many nations offer long-term fixed rates, though penalties for early repayment (such as selling the house before the term ends) can be significantly more punitive than in the US.

Navigating the Rate Lock

Given that financial markets are in a state of constant flux, mortgage rates can change daily, or even hourly. To protect borrowers from a sudden spike in rates during the closing process, lenders offer a “rate lock.”

A rate lock is a guarantee from the lender to honor a specific interest rate for a set period—typically 30 to 60 days—while the loan application is processed. If market rates rise during this period, the borrower is protected. If rates fall, the borrower is usually bound to the locked rate, unless their agreement includes a “float-down” provision. Understanding the terms of a rate lock is critical, particularly in volatile economic climates where a fraction of a percentage point can alter purchasing power.

Historical Context and Future Outlook

To understand the current rate environment, one must view it through a historical lens. In the early 1980s, amidst efforts to curb runaway inflation, U.S. mortgage rates peaked at over 18%. Conversely, following the 2008 financial crisis and the COVID-19 pandemic, rates plummeted to artificial lows, dipping below 3% due to aggressive quantitative easing by central banks.

Today’s borrowers must adjust their expectations to a normalized environment. The ultra-low rates of the recent past were an anomaly, not the rule. As economies stabilize, rates tend to revert to averages that reflect real inflation and growth expectations.

Conclusion : The Strategic Borrower

Securing a mortgage is not merely a transactional step in buying a home; it is a strategic financial decision with multi-decade implications. The interest rate obtained determines the total cost of the asset and the monthly strain on a household’s budget.

For the modern homebuyer, the goal should not simply be to find the absolute lowest advertised number, but to understand the interplay between the rate, the APR, the loan term, and their personal financial horizon. By maintaining a strong credit profile, understanding the influence of macroeconomic trends, and distinguishing between fixed and adjustable products, borrowers can navigate the complexities of mortgage rates with confidence. In a market defined by data, the well-informed borrower possesses the ultimate leverage.