For prospective homeowners and current mortgage holders alike, the stated interest rate on a loan is often viewed as a singular, monolithic figure that determines affordability. Yet, this number is actually a complex derivative representing the confluence of global economic forces, monetary policy decisions, and investor sentiment. To the untrained observer, the fluctuations may seem arbitrary, but they follow a discernible, albeit intricate, logic.

Understanding the machinery beneath housing finance is essential for navigating the market. It requires dispelling the common myth that rates are arbitrarily set by loan officers or even directly dictated by a central government agency. Instead, mortgage rates are prices determined in vast, liquid capital markets, reacting in real-time to the evolving health of the broader economy. A fundamental misunderstanding of why mortgage rates go up or down influences financial decisions that last for decades. To comprehend these movements, one must examine the primary drivers: inflation, the bond market, central bank activity, and overall economic growth.

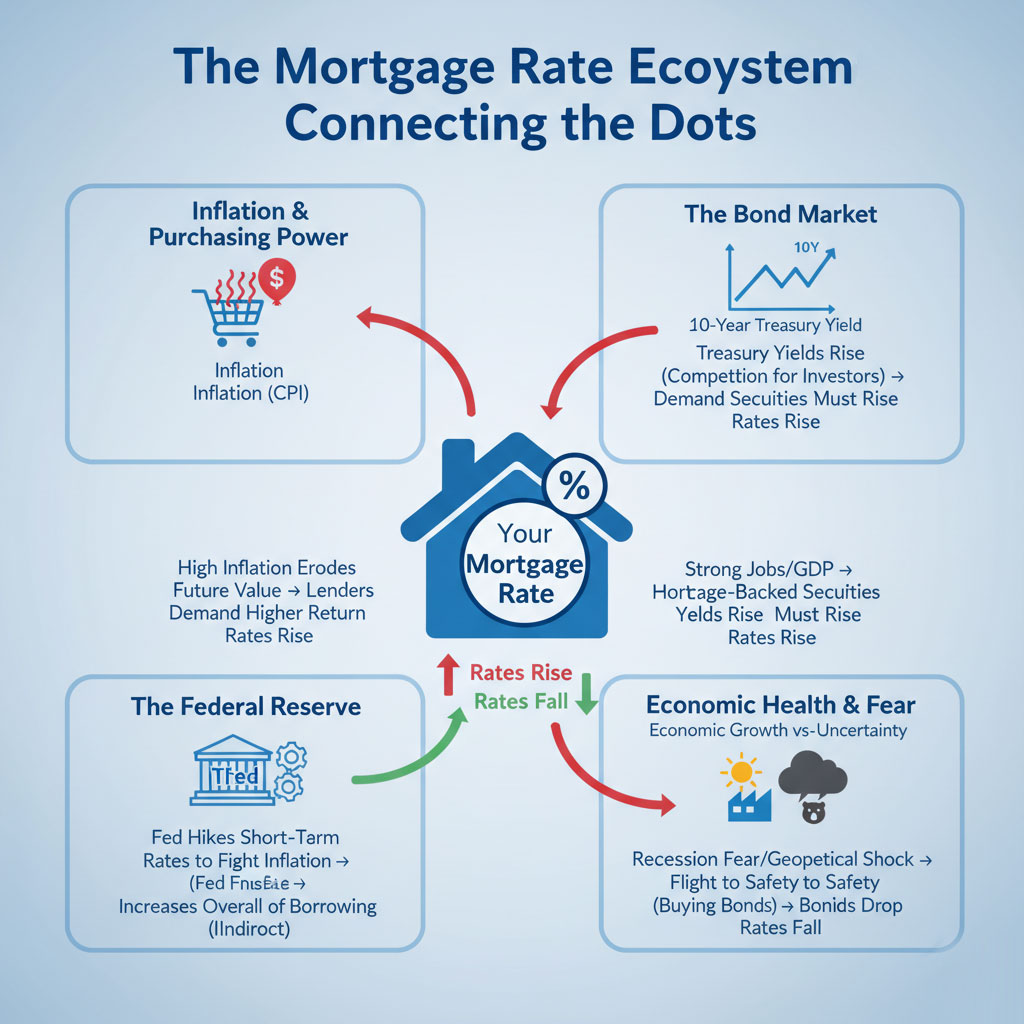

The Invisible Hand of Inflation

If there is a single gravitational force that exerts the most significant pull on long-term mortgage rates, it is inflation. Inflation erodes the purchasing power of money over time. For a lender, this is a critical risk.

When a bank or financial institution lends money for a 30-year mortgage at a fixed rate, they are essentially betting on the future value of that currency. If a lender provides a loan at 4% interest, but annual inflation is running at 3%, their “real” rate of return—the actual increase in purchasing power they gain—is only 1%. If inflation accelerates to 5%, that lender is effectively losing purchasing power on the loan, despite the nominal interest payments.

Therefore, when inflationary pressures mount—indicated by reports like the Consumer Price Index (CPI) showing rising costs for goods and services—lenders must adjust upward. They demand higher interest rates to compensate for the anticipated erosion of the money’s value by the time it is repaid in future years. Consequently, when assessing why mortgage rates go up or down, inflationary pressure acts as the primary accelerant. Conversely, when inflation cools and prices stabilize, lenders feel more secure offering lower rates, as the risk of currency devaluation diminishes.

The Crucial Link: The 10-Year Treasury Yield

While inflation is the theoretical driver, the practical, day-to-day benchmark for fixed mortgage rates is the bond market, specifically the yield on the 10-Year U.S. Treasury note.

Mortgages and U.S. Treasury bonds are competitors for investor capital. U.S. Treasuries are considered risk-free assets because they are backed by the full faith and credit of the United States government. Mortgages, even when packaged into highly rated Mortgage-Backed Securities (MBS), carry a slightly higher risk (prepayment risk or default risk). Therefore, to attract investors, mortgages must offer a higher yield—or interest rate—than the risk-free Treasury note.

Historically, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield hovers around 1.5 to 2 percentage points, though this changes based on market volatility. When economic news causes investors to sell Treasury bonds, the price of those bonds drops, and their yield rises. Because mortgages must compete with these higher yields to attract capital, mortgage rates follow suit. The 10-year Treasury yield is perhaps the most reliable bellwether for predicting whether mortgage rates go up or down in the near term. If you see the 10-year yield spike on a financial news ticker, it is virtually guaranteed that mortgage lenders are re-pricing their loan offerings upward almost immediately.

The Federal Reserve’s Pivotal, Indirect Role

A persistent misconception among the general public is that the Federal Reserve directly sets mortgage rates. It does not. The Fed’s primary tool is the Federal Funds Rate, which is a short-term rate for overnight lending between banks.

However, the Fed’s influence over mortgage rates is profound, even if indirect. The Federal Reserve has a dual mandate: to maximize employment and keep prices stable (control inflation). When inflation runs too high, the Fed engages in monetary tightening by raising the Federal Funds Rate. This makes borrowing more expensive for banks, a cost which ripples through the entire economy, eventually pushing up longer-term rates, including mortgages.

Furthermore, the Fed influences rates through its balance sheet operations, known as Quantitative Easing (QE) or Quantitative Tightening (QT). During economic crises, the Fed may buy massive amounts of Mortgage-Backed Securities and Treasury bonds to inject liquidity into the market. This high demand keeps bond prices high and yields—and therefore mortgage rates—low. Conversely, when the Fed steps back and allows these securities to roll off its balance sheet (QT), it increases the supply on the open market, exerting upward pressure on yields. While not a direct dial, their actions create the environment where mortgage rates go up or down based on their stance toward economic heat.

To summarize these complex interactions, consider the following table detailing how primary indicators typically influence rate movement.

Why Mortgage Rates Go Up or Down?

| Economic Indicator | What It Measures | Typical Impact on Mortgage Rates | Underlying Mechanism |

|---|---|---|---|

| High Inflation (CPI/PCE) | The rate at which prices for goods/services are rising. | Rates Go Up | Lenders demand higher yields to offset the eroding future purchasing power of the repayments. |

| Rising 10-Year Treasury Yield | The return investors get for lending to the U.S. govt for a decade. | Rates Go Up | Mortgages compete with Treasuries for investors; as risk-free yields rise, mortgage yields must rise to remain attractive. |

| Fed Hikes Federal Funds Rate | The cost of short-term, overnight borrowing for banks. | Rates Go Up (Indirectly) | Increases the baseline cost of money in the economy, eventually filtering up to long-term lending rates. |

| Strong Jobs Report / High GDP | Overall economic health and labor market tightness. | Rates Tend to Rise | A strong economy often leads to higher wages and spending, fueling inflation concerns and reducing the need for safe-haven bonds. |

| Geopolitical Crisis / Recession Fear | Global instability or fear of economic contraction. | Rates Tend to Fall | Investors flee risky assets (stocks) and buy safe assets (bonds), driving bond prices up and yields (and mortgage rates) down. |

Economic Vigor and Global Uncertainty

Beyond central banks and inflation data, the general trajectory of economic growth plays a significant role. In a robust, expanding economy, demand for credit increases. Businesses borrow to expand, and consumers borrow to buy homes and cars. This increased demand for capital, coupled with the inflationary pressures that often accompany a hot economy, tends to push interest rates higher. Strong employment reports, rising wages, and high Gross Domestic Product (GDP) growth are generally harbingers of rising rates.

Conversely, signs of economic weakness—rising unemployment, stalling GDP, or fears of a recession—usually lead to lower rates. In such times, demand for borrowing cools. Furthermore, economic uncertainty often triggers a “flight to safety” among global investors. When investors are nervous about the stock market or geopolitical instability, they tend to move capital into safe-haven assets, primarily U.S. Treasury bonds. As discussed, huge buying pressure on bonds drives down yields, taking mortgage rates down with them.

The Secondary Mortgage Market: The Plumbing of Housing Finance

Finally, one must understand the mechanics of the “secondary market.” When a borrower closes on a loan with a local bank or non-bank lender, that lender rarely keeps the loan on its books for 30 years. Instead, they sell the loan into the secondary market, largely to government-sponsored enterprises like Fannie Mae and Freddie Mac. These loans are then pooled together into Mortgage-Backed Securities (MBS) and sold to global investors—pension funds, insurance companies, foreign governments, and hedge funds.

The appetite of these global investors for MBS determines the final rate a borrower pays. If investors perceive higher risks in the housing market, or if they have better investment alternatives elsewhere, they will demand a lower price for MBS, which translates to higher yields and higher mortgage rates for consumers. The smooth functioning of this secondary market is vital; any disruption in the “plumbing” can cause rate volatility unrelated to standard economic data.

Navigating the Rate Landscape

Mortgage rates are never static; they are a real-time reflection of the cost of capital in a globalized economy. They cycle through periods of historic lows, as seen in the years following the 2008 financial crisis and the COVID-19 pandemic, and revert to higher averages during periods of intense inflation or economic normalization.

For consumers, trying to time the absolute bottom of a rate cycle is a notoriously difficult, if not impossible, endeavor given the multitude of variables at play. Recognizing that these rates are tied to broader economic health, rather than arbitrary decisions, provides a necessary perspective for long-term financial planning. Ultimately, understanding the mechanics of why mortgage rates go up or down provides crucial context, moving the decision to finance a home away from speculation and toward a calculation of long-term affordability relative to the economic environment.