Fixed-Rate vs Adjustable-Rate Mortgages : Which Is Better for You? The decision of how to finance a home is rarely merely an arithmetic calculation; it is a fundamental assessment of risk tolerance placed against the backdrop of macroeconomic forces. For decades, the central tension in residential lending has centered on the choice between rate certainty and initial affordability. This dialectic—Fixed-Rate vs Adjustable-Rate Mortgages—remains the critical juncture for prospective homebuyers globally, a decision complicated significantly by the end of the ultra-low interest rate era.

In the current economic landscape, defined by central banks combating persistent inflation through aggressive monetary tightening, the stakes of this choice have crystallized. The comforting predictability of a fixed payment is now priced at a premium, while the lower introductory rates of variable products carry the palpable threat of future payment shock. Understanding the mechanics of these financial instruments, and their distinct regional variations between North American and European models, is essential for navigating modern homeownership.

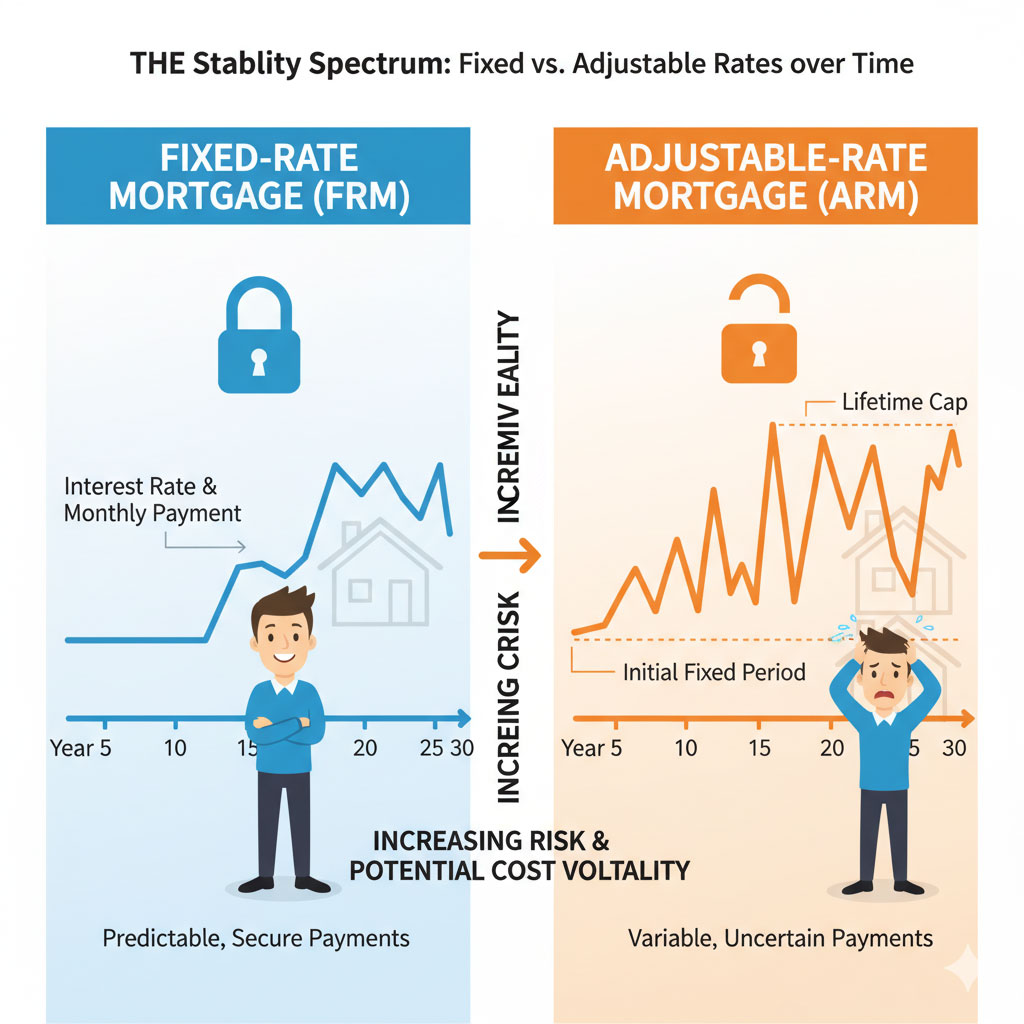

The Architecture of Certainty: The Fixed-Rate Mortgage (FRM)

The Fixed-Rate Mortgage is the bedrock of conservative financial planning in real estate. Its premise is elegant in its simplicity: the interest rate determined at the loan’s inception remains invariant for the entire life of the product, regardless of subsequent fluctuations in the broader financial markets.

In the United States, the 30-year fixed-rate mortgage is a unique cultural and financial phenomenon, largely made possible by government-sponsored enterprises like Fannie Mae and Freddie Mac that securitize these long-term risks. For the borrower, it offers unparalleled immunity to interest rate volatility. Every monthly payment is composed of principal and interest in a precise, amortization schedule that guarantees the loan is fully paid off by the end of the term.

The primary advantage here is budgetary predictability. In an environment where the Federal Reserve has rapidly elevated the federal funds rate, holding a legacy fixed-rate mortgage at 3% while current market rates hover near 7% represents a significant financial asset for existing homeowners—a phenomenon currently contributing to reduced housing inventory liquidity.

However, this certainty is not free. Lenders must price in decades of inflation and interest rate risk. Therefore, fixed rates are almost invariably higher than the initial rates offered on adjustable products at the time of origination. The borrower pays a premium for peace of mind, effectively purchasing insurance against rising rates.

The Mechanics of Risk: Adjustable and Variable-Rate Mortgages

Conversely, Adjustable-Rate Mortgages (ARMs) in the U.S., and their counterparts, Variable-Rate Mortgages (VRMs) in Canada and the UK, introduce an element of dynamism—and risk—into household finances.

These products typically begin with a “teaser” or initial fixed period during which the interest rate is lower than prevailing fixed-rate mortgages. This initial period can range significantly, from as short as six months to as long as ten years. Once this period expires, the loan enters its adjustment phase.

The new rate is calculated based on a pre-determined formula: an underlying benchmark index (such as the Secured Overnight Financing Rate, or SOFR, in the U.S., or the central bank base rate elsewhere) plus a fixed “margin” set by the lender. As the benchmark index moves in response to central bank policy and market conditions, the borrower’s interest rate—and monthly payment—fluctuates accordingly.

Protective Measures and Payment Shock

To mitigate the terrifying prospect of unlimited rate increases, U.S. ARMs almost always include rate caps. These caps limit how much the interest rate can increase during a single adjustment period and over the lifetime of the loan. For example, a “5/1 ARM with 2/2/5 caps” means the rate is fixed for five years, adjusts annually thereafter, cannot increase more than 2% in the first adjustment, no more than 2% in subsequent years, and never more than 5% above the initial start rate.

While caps provide a safety net, the potential for payment shock remains real. If an ARM resets during a period of aggressively hawkish monetary policy, homeowners can see their monthly obligations surge by hundreds or even thousands of dollars overnight, straining household liquidity and increasing default risk.

A Transatlantic Divide: Regional Nuances in Lending Models

It is critical to contextualize the Fixed-Rate vs Adjustable-Rate Mortgages debate geographically, as the terminology and product structures differ radically between the United States and major Commonwealth economies like the UK and Canada.

In the U.S., a “fixed-rate” truly means the rate is locked for the entire 15 or 30-year amortization period.

In the UK and Canada, however, what is often marketed as a “fixed-rate mortgage” is structurally closer to a U.S. hybrid ARM. A UK borrower might take a “five-year fix,” guaranteeing their rate for 60 months. The amortization period, however, might be 25 years. At the end of that five-year term, the borrower does not merely face a rate adjustment; their loan contract effectively ends, and they revert to the lender’s typically much higher Standard Variable Rate (SVR).

This structure forces Canadian and UK homeowners to periodically “remortgage” or refinance. Consequently, these homeowners carry significant “refinancing risk”—the danger that when their short-term fixed deal expires, prevailing market rates will be substantially higher. This dynamic makes these housing markets far more sensitive to central bank rate hikes in the near to medium term compared to the U.S. market, where many homeowners are insulated by long-term fixed rates secured years ago.

Analytical Comparison: The Decision Matrix

Choosing between these paths requires an honest appraisal of one’s financial horizon and risk appetite. The decision is rarely about outsmarting the market; it is about aligning debt structure with life plans.

When evaluating Fixed-Rate vs Adjustable-Rate Mortgages, the analysis often hinges on the intended duration of homeownership. If a borrower is certain they will sell the property or pay off the loan before an ARM’s initial fixed period expires, the adjustable product can offer substantial interest savings with minimal theoretical risk.

Below is a summary of the structural differences and strategic considerations inherent in these mortgage types globally.

Fixed-Rate vs Adjustable-Rate Mortgages

| Feature | US 30-Year Fixed-Rate Mortgage (FRM) | US Hybrid Adjustable-Rate Mortgage (e.g., 5/1 ARM) | UK/Canada “Fixed-Rate” (e.g., 5-Year Term) | UK/Canada Variable-Rate Mortgage (VRM) |

|---|---|---|---|---|

| Rate Certainty | Absolute for full loan life (e.g., 30 years). | Limited to initial period only (e.g., 5 years). | Limited to the contractual term (e.g., 2-5 years). | None. Rate fluctuates with the prime/base rate immediately. |

| Initial Interest Rate | Typically highest at origination due to priced-in long-term risk. | Lower initial “teaser” rate compared to 30-year FRM. | Moderate. Lower than long-term US fixed, higher than immediate variable. | Typically the lowest initial option, but immediately volatile. |

| Rate Adjustments | None. | Adjusts periodically (e.g., annually) after the initial fixed phase, based on index + margin. | The rate does not adjust; the contract ends, forcing a refinance at new market rates. | Adjusts swiftly, often the month following a central bank rate change. |

| Protections | N/A (Rate is static). | Rate Caps (Periodic and Lifetime limits on increases). | None at renewal. Borrower faces full market exposure upon term expiry. | No specific caps on rate movement; payments increase or principal repayment slows. |

| Primary Risks | Paying above-market rates if rates drop significantly (opportunity cost). | “Payment Shock” upon reset if index rates have soared. | “Refinancing Risk” every few years; vulnerability to rate spikes at renewal. | Immediate cash-flow volatility; potential for negative amortization in some Canadian products. |

| Best Suited For | Long-term homeowners prioritizing stability and budgeting certainty above all else. | Borrowers planning to sell or refinance before the fixed period ends; those with high risk tolerance. | The standard option in these regions; requires active management and refinancing strategy. | Sophisticated borrowers expecting rates to fall soon or those with substantial cash flow buffers. |

The Macroeconomic Gamble

Currently, the debate over Fixed-Rate vs Adjustable-Rate Mortgages is heavily influenced by the forward guidance of central banks. After a historic tightening cycle, many economists anticipate a stabilization or eventual lowering of interest rates in the coming years as inflation cools.

This outlook complicates the decision. Locking in a 30-year fixed rate at today’s elevated levels could mean overpaying for decades if rates significantly retreat. Conversely, choosing an ARM today in anticipation of falling rates is a gamble. If inflation proves entrenched and rates remain “higher for longer,” the ARM borrower faces the painful reality of upward adjustments.

Ultimately, the fixed-rate mortgage remains the prudent choice for the risk-averse homeowner seeking to immunize their largest monthly expense against economic turbulence. The adjustable-rate mortgage serves as a specialized tool for those with shorter time horizons or significant financial liquidity who are willing to wager on a benign interest rate environment in exchange for lower initial costs.